Are RWA protocols actually succeeding? Financial Analysis 📊 | RWA Part2

Are RWA protocols actually succeeding? Financial Analysis 📊 | RWA Part2

Is the narrative going to keep the pace? Is the business model actually sustainable?

In Part 1 of this deep dive into Real World Assets we saw:

• 🌍 Overview of the ecosystem

• 🏢 Enterprises and Countries betting on RWA

For getting a good context of what we are gonna delve into visit the link below 👇

This second part will be focused on money: How much demand this protocols are getting, its business models and what (if there are) big firms are putting some serious money for profiting or help thriving this ecosystem. All this can be summarized in the following points:

• 💰 Money at stake | Financial Analysis

• 🔄 Comparison between RWA and Crypto Assets

Without further ado, let's get started.

Introduction

⚠The integration of real-world assets onto blockchain networks is a complex process that involves both on-chain and off-chain components. It requires careful consideration of legal, regulatory, technical, and operational aspects to ensure that the tokens accurately represent the underlying assets and comply with applicable laws and regulations. Nobody wants to hold a representation of a Rolex Cosmograph Daytona that does not exist anymore, which is actually one of my biggest concerns and that’s the reason why I believe Custodians and DONs (Decentralized Oracle Networks) will play a key and vital role in this industry.

🗒️ Remember that this kind of assets are NOT native to the blockchain. They undergo a tokenization process through a third party for subsequent use in DeFi or their simple representation (with all the benefits that entails) on a blockchain.

At present, most protocols that in any way interact with or offer RWAs to clients must require them to have KYC, or in other words, to be Accredited Investors, and it is precisely the data that KYC provides us (since these investors will have an on-chain identity) together with the transparency of the blockchain that will allow us to take the pulse of this sector of the industry.

🧵 I’ll delve into how to extract valuable alpha by exploring KYC’ed people in the blockchain since they are investors who are generally more financially experienced than the average and have a larger amount of capital. Follow me on X so you don't miss it.

💰 Money at stake | Financial Analysis

Market Sectors

🏛Credit Protocols (RWA lending)

💵T-Bills issuers

🏘Fragmented Real State

Credit Protocols

Credit protocols facilitate originations, deal funding, and borrower repayments.

This sector currently has +$550M in active loans yielding on average a ~10% APR with the TOP 3 protocols being:

Quick overview as of 18th September 2023

Centrifuge

Active Loans → $238,212,641🟢

APY → 8.86%

Fees earned → $0 (Protocol does not currently earn money from its business) ‼

Is it paying rewards? → Yes ✅

Had the protocol defaulted loans? → Yes ($13,211,674) 🔴

Centrifuge boasts a substantial amount of active loans and offers an attractive APY. However, it's important to note that the protocol isn't generating fees from its operations. Despite paying rewards, Centrifuge has encountered loan defaults, which raises questions about its risk management strategies.

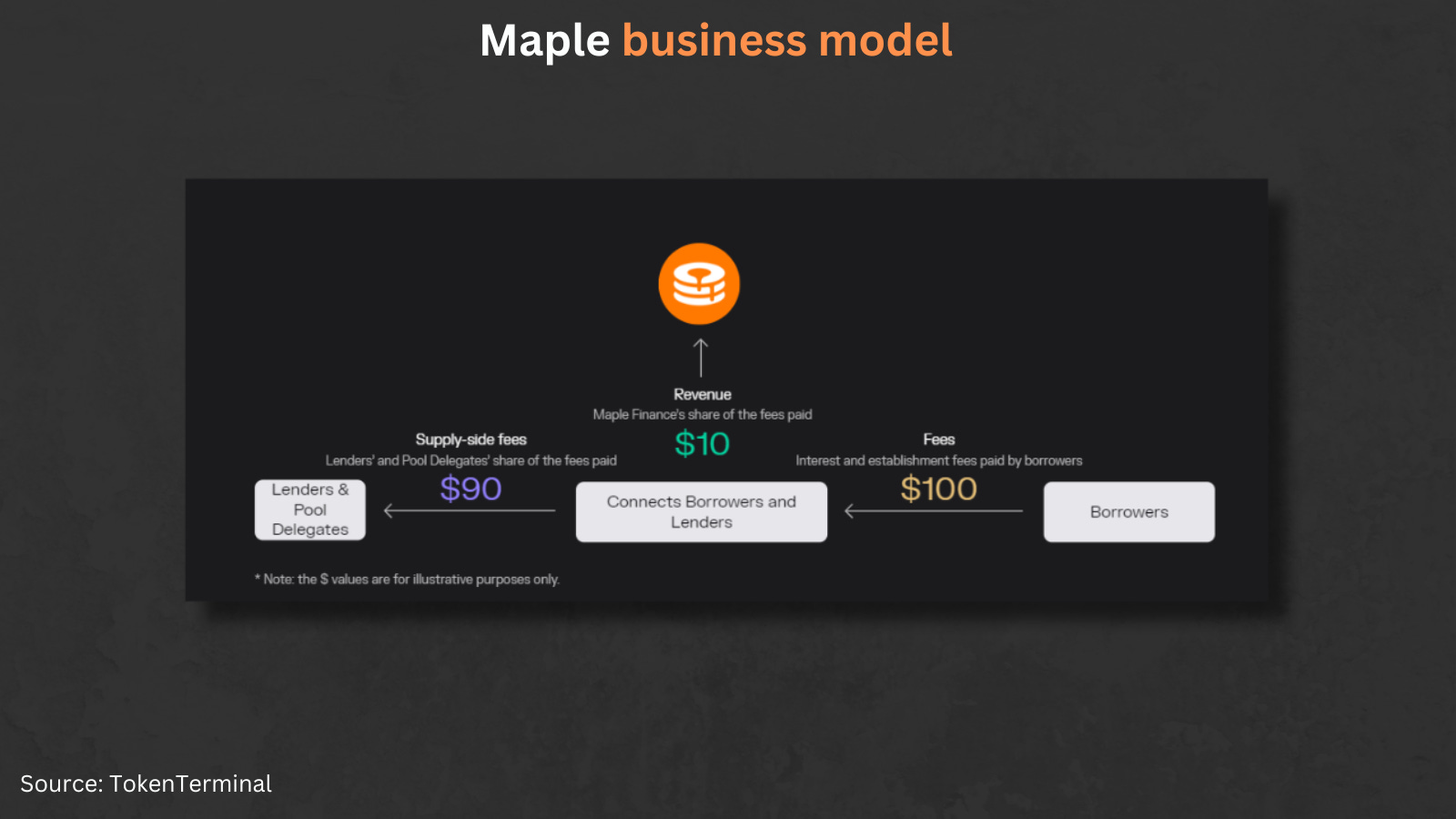

Active Loans → $130,458,229 🟢

APY → 8.32%

Fees earned → $3,686,104 💰

Is it paying rewards? → No ❌(maybe they don’t find worthy the costs/rewards of incentives)

Had the protocol defaulted loans? → Yes ($47,470,568) 🔴

Maple, on the other hand, has managed to generate substantial fees from its active loans. However, it's worth noting that they are not currently offering rewards, which might impact their user base. The significant default amount also calls for a closer examination of their risk assessment and mitigation strategies.

Active Loans → $103,754,392 🟢

APY → 11.06%

Fees earned → $2,290,689 💰

Is it paying rewards? → Yes ✅

Had the protocol defaulted loans? → Yes ($5,000,000) 🔴

Goldfinch offers an enticing APY and has successfully generated fees from its active loans. Additionally, they provide rewards to users, which can attract more participants. Nevertheless, their defaults are not negligible, and it's essential to understand how they intend to address this issue.

For those who like a table format:

Now, some questions arise:

How do these protocols plan to improve risk management and reduce loan defaults?

What strategies do they have in place to incentivize users and attract more liquidity, especially in the case of Maple, which currently does not offer rewards?

Can Centrifuge find a sustainable way to generate fees and ensure its long-term viability in the DeFi space?

T-Bills Issuers

Tokenized US Treasuries have seen a surge in popularity, attracting a wide range of players, from established $100 billion+ asset management firms to innovative young startups.

This sector currently has a Total Value of +$630M providing investors an average interest of 5.25% with an average maturity of the underlaying T-Bills being ~2 months (0.182 years)

Quick Overview of the TOP 3 Protocols:

Franklin OnChain U.S. Government Money Fund

Ticker → $FOBXX

Market Cap → +$280M between Stellar and Polygon 🟢

Yield to maturity → 5.19%✅

Weighted Average Maturity → 19 days (0.052 years) 💨

Manager (who manages the assets) → Franklin Templeton

Franklin OnChain U.S. Government Money Fund boasts a substantial market cap across multiple blockchains. Its attractive yield to maturity and short average maturity make it an appealing choice. However, questions arise regarding how Franklin Templeton manages the underlying assets (I couldn’t find info about that) and whether they have a robust security and risk management strategy in place.

Ondo

Ticker → $OUSG

Market Cap → +$164M between Ethereum and Polygon 🟢

Yield to maturity → 5.37%✅

Asset Distribution → 3.79% AA Rated and 96.21% Cash and/or Derivatives

Weighted Average Maturity → ~3 months (0.28 years)

Manager (who manages the assets) → Ondo

Ondo stands out with its diverse asset distribution, including a portion of AA-rated assets. Its yield to maturity is competitive, but the longer average maturity warrants a closer look at how they mitigate interest rate risks. Additionally, understanding the nature of their cash and derivative holdings is essential for assessing risk.

Matrixdock

Ticker → $STBT

Market Cap → ~$84M on Ethereum🟢

Yield to maturity → 5.21%✅

Asset Distribution → 87.46% Repo and 12.54% T-bills

Weighted Average Maturity → ~3.6 days (0.0099 years) 💨

Manager (who manages the assets) → Matrixdock

Contract Address → Ethereum

Matrixdock garners attention with its solid market cap on the Ethereum blockchain. Its primary asset distribution in repos and T-bills indicates a focus on low-risk assets. The ultra-short average maturity allows for almost instant liquidity and payment of interest at maturity. We will see how this strategy works in the long term as it involves constant asset management.

Table format:

Fragmented Real State

Thanks to blockchain, property ownership is broken down into tradable tokens, bringing you closer to the action. This innovation not only boosts liquidity but also enhances risk-return dynamics, offering everyday investors like you exciting access to a lucrative asset class. Welcome to a new era in investing in Real State.

The truth is that as a relatively new and little explored sector, together with the fact that the few protocols within this sector are not transparent about the data, or at least I have not been able to find them after hours of research, I have only been able to find data from the leading protocol

As we can see it is a sector with a strong capital inflow trend (+$90M in sales), which indicates that they have more and more properties (401 at the time of writing this) and that they are sold relatively easily having attracted 16652 landlords who are obtaining an average return of ~7%. It should be noted that RealT has a section (fork of Aave) in which you can borrow against tokens of the houses as collateral, with $9.3M deposited and $2.8M in loans.

Tokenized and fractionalized real estate presents a promising avenue for diversifying investment portfolios and increasing accessibility to the real estate market. However, investors should carefully weigh these advantages against the potential tradeoffs and consider their risk tolerance, regulatory requirements, and investment goals before venturing into this emerging sector.

Tradeoffs I’m monitoring:

Regulatory Complexity: The regulatory environment for tokenized real estate is evolving and can be complex. Investors need to navigate compliance issues, which can vary by jurisdiction.

Fractional Ownership Challenges: Coordinating decisions among numerous fractional owners can be challenging. This includes decisions related to property management, rent distribution, and asset maintenance.

Lack of Physical Control: Token holders typically don't have direct control over the physical property. They rely on third-party property managers, which can introduce risks if not managed properly.

Technology Risks: Dependence on blockchain technology means exposure to potential smart contract bugs, security breaches, or platform failures.

Illiquid Tokens: While tokenization offers increased liquidity compared to traditional real estate, some tokens may still be illiquid, especially for niche or less popular properties.

Some other data

Maker’s Real-World Asset exposure

And underlaying companies

At this time there are 15 companies with Vaults that provide some form of RWA as collateral and in exchange they get DAI based on the stipulated Loan-To-Value. The parameters and authorizations of the agreement between "Company"-Maker go through the governance of the DAO itself, where they decide parameters such as:

Example: RWA-008 Societe Generale – Forge (OFH) Onboarding

Stability Fee: 0.05% → Fees to be paid for the issuance of DAI

Debt Ceiling: 30 million DAI → Maximum number of DAI to be issued

Liquidation Ratio: 100% → % of liquidation

Debt write-off timelock (tau): 0

Liquidation Process: See MIP21 for details.

Currently, Real World Assets compose the following within Maker:

⚖Balance Sheet: $2.965B worth of RWA, this amount is broken down in the first image below and it constitutes +54% of all the assets in the balance sheet.

💵Revenue: +$111M are generated by RWA and accounts for +63% of Maker's entire revenue. For context in went from less than 10% to the actual levels in one year.

🏛The biggest player within this is Vault MIP65 corresponding to Monetalis Clydesdale with more than $1.161B broken down into Cash, T-Bills and ETFs, having generated since inception +$26.2M in revenue and +$11.3 paid to MakerDAO. All this information is public and can be viewed in this Dune Dashboard that tracks its balance sheet.

🔄 Comparison between RWA and other crypto assets

Now that we've analyzed the data related to traditional assets incorporated into blockchain technology and their contributions to DeFi protocols, it's time to compare them with assets that are native to blockchain itself.

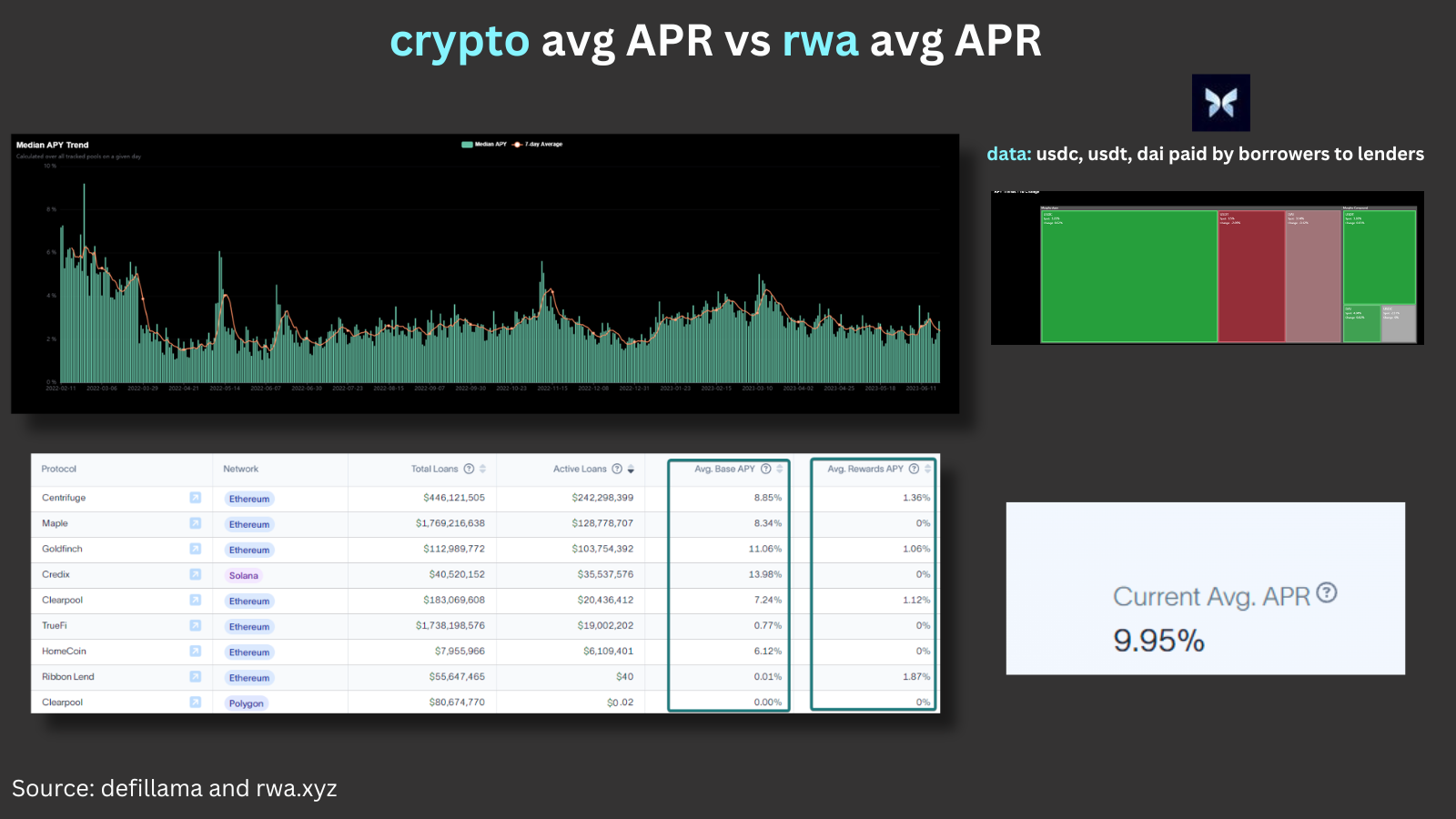

Offerings by Decentralized Lending Protocols vs Private Credit Protocols

For the purpose of this point I’m gonna compare (i) APR paid by the borrower and (ii) APR paid to the supply side (lenders).

I choose Morpho as a representative of decentralized protocol since it encompasses the leading lending protocols and optimizes their performance by offering better offers and yields to both parts.

As for the RWA protocols, the rwa.xyz website itself averages what borrowers pay to open a loan in the different protocols.

📉Average APR paid by the borrowers to lenders in Morpho (DeFi): 2.4%

📈Average APR paid by the borrowers to lenders in RWA lending protocols: 9.95%

Looking at this data you may think that no, DeFi protocols cannot compete with the interest generated by private credit protocols, not to mention that to generate a similar yield DeFi protocols generally use their own tokens that end up devaluating 90%.

However, the truth is that the analysis of what is better or worse goes far beyond who offers a higher yield. Just tell that to all the Luna Survivors of 2022 (including myself). To understand what an investor needs or wants, you have to take into account things such as:

🛡Risk Assessment: Understanding the Variances

When it comes to risk, distinguishing between off-chain and on-chain assets is crucial. Off-chain assets generally carry a lower risk of default compared to their on-chain counterparts. However, it's important to note that the control exerted by the protocol over off-chain assets is relatively weaker, primarily due to the absence of smart contracts in various stages of the loan process.

As a result, when participating in an RWA lending protocol, you are essentially taking on a heightened level of risk. This elevated risk can be attributed to the uncertainty surrounding the use of the loan proceeds. Borrowers typically allocate these funds to ventures known for their inherent risks, such as startup funding or technology development. It's this elevated risk profile that justifies the average interest rate of 9.95% – a reflection of the risk associated with such ventures.

⚖Collateralization: Balancing Efficiency and Safety

When it comes to collateralization, a notable difference emerges between DeFi protocols and traditional financial (TradFi) systems. In DeFi, collateralization requires users to lock up more capital than the amount they intend to borrow. This is primarily done to ensure the financial stability and health of the protocol. Interestingly, DeFi platforms do not require users to present any form of credit history, making it more accessible.

However, this approach does come with a tradeoff. The requirement to over-collateralize loans in DeFi means that capital is utilized less efficiently compared to the collateralized or under-collateralized loans often seen in traditional finance (TradFi). In TradFi, borrowers may be able to access larger loan amounts relative to their collateral, which can be advantageous for capital efficiency.

To conclude, DeFi's approach to collateralization emphasizes safety and accessibility but may result in less capital efficiency compared to the collateralized or under-collateralized loans prevalent in traditional financial systems.

Conclusion:

The future of Real World Assets (RWAs) on the blockchain is poised for a transformative journey. This integration promises to democratize access to traditionally illiquid assets, expanding the horizons of decentralized finance.

Advancements in tokenization and governance are paving the way for a world where real estate, commodities, and revenue streams coexist seamlessly with cryptocurrencies and smart contracts. However, regulatory clarity, risk management, and scalability remain challenges.

Despite the hurdles, the fusion of RWAs with on-chain technology represents a revolutionary shift in finance. It offers new opportunities for individuals and institutions to reimagine how we interact with and trade the assets underpinning our financial world.

Thanks for reading, until next time.

“Second-level thinkers know that to achieve superior results, they have to have an edge in either information or analysis, or both.” - Howard S. Marks