Real World Assets (“RWAs”) are assets that exist off-chain but are tokenized and brought on-chain to be used as a source of yield within DeFi.

Fixed income is the predominant market in the RWA space.

RWAs can offer yields to DeFi which are sustainable, reliable, and backed by traditional asset classes.

RWAs can render DeFi to become more compatible with external markets, resulting in greater liquidity, capital efficiency, and investment opportunities.

RWAs allow DeFi the ability to bridge the gap between decentralized financial systems and traditional financial systems.

Now that we know how and why T-Bills and other debt instruments are worth using at DeFi, let's see the numbers behind this:

We are gonna focus on data provided by those protocols that are doing a great job on being transparent and that are attracting decent liquidity, and those are:

44 accounts (or individuals) have deposited a total of $140M in the protocol. In addition, $OUSG(Ondo Short-Term U.S. Government Bond Fund) can be used inFlux Finance, allowing for greater capital efficiency by borrowing USDC, DAI, FRAX or USDT(!!You have to own OUSG to borrow stablecoins)

It should be noted that Flux Finance (its contract) is the main holder of $OUSG (+404K), which had been deposited on the platform by investors in order to take advantage of it.

I recommend you take a look at $OUSG holders (and generally all these tokens) and Flux users as they are accredited investors whose portfolios can be viewed in a block explorer to see where and what they are investing in. There is some really interesting stuff 👀

As of today it is the project that has attracted the most users of Tokenized Public Securities (Bonds) with 94 accounts. Is it because it is easier to register on the platform, or because it has a liquidity pool in Curve with +$16M against 3CRV offering a return of 5-14% in $CRV? (at time of writing this) As far as I'm aware anyone can deploy capital into this pool (Convex or Curve) and get exposure to STBT without passing KYC.

It has 31 holders, and may be one of the fastest growing early stage projects due to the removal of commissions at this stage of development. It does not have much composability in DeFi at least for the time being, so not much data can be said about this token (this may be due to the fact that it can only be transferred to whitelisted wallets).

These protocols are currently used by people with much more capital than the average investor (you have to be an authorized investor to access these products), so it may be one of the next hot topics in the industry, as it is attracting liquidity at a decent pace, and good partnerships with different DeFi protocols may emerge. It's a win-win scenario.

💡 Bankruptcy Remote: at least Ondo and OpenEden (I have not been able to find the same information with Matrixdock) are based on a different legal structure than what we are used to seeing in stablecoins, the main difference being that the tokenholder is the holder of the backing asset in case of bankruptcy and not the company. Tokens are fully segregated and held with qualified custodians which are regulated and insured.

We will return to T-Bills for the last part where we will see the convergence between these assets and crypto assets by comparing them.

Let's see what Private Credit is playing out within DeFi:

Private Credit ($556M in active loans)

Credit lines, a fundamental pillar of the global economy, are at the epicenter of this financial evolution. With the integration of Private Credits into DeFi space, the gates are opening to a new era of inclusive access, transparency and efficiency in the credit world. We will explore how these two converging forces can unleash a torrent of opportunities for entrepreneurs, investors and borrowers alike. Barriers to credit access are fading and possibilities are multiplying.

as an example, which is on a mission to expand access to capital by creating a single global credit marketplace that allow people to borrow from the same capital markets and that all investors can access those deals directly, dealing with the fragmentation problem of the financial system.

In other words it allows for crypto borrowing without crypto collateral—with loans instead fully collateralized off-chain.

Most protocols focused on this business are based on the following premise:

An on-chain marketplace focused exclusively on serving Institutional and Individual Accredited Investors with high-quality lending opportunities which suit their liquidity, risk and return requirements.

In order to avoid distracting from the main topic of this article, I will limit myself to sharing how such a protocol would work as well as resources for you to learn how it works in more detail.

As lending operations occurs on-chain we can analyze what is behind this business, such as which institutions, countries or simply wallets are using this type of services.

📊 Data:

On a general and historical view, 1723 loans have been taken for a whopping value ~$4.5B. As of right now data is the following:

Active loans: +$550M;

🛒Consumer → $184M

🚗 Auto → $175M

💻Fintech → $105M

Current Average APR: 10.63%

📈 What are the best performing protocols?

To answer this question we will base the analysis on (i) Total Loans taken (to see how much demand the protocol has had and why) (ii) Active Loans(to see the current demand for the protocol and what changes there have been historically, if any).

Total Loans and Active Loans:

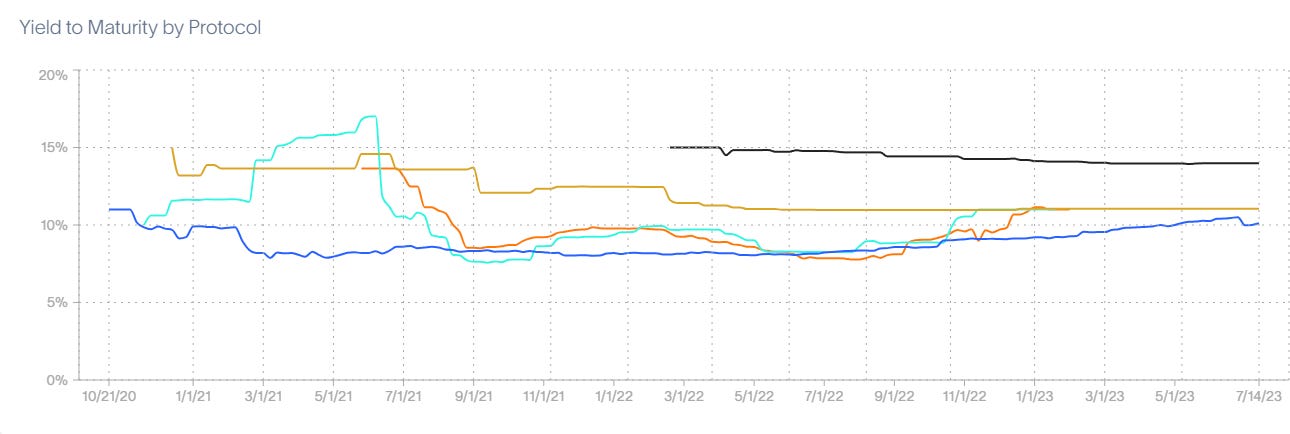

Maple, TrueFi and Centrifuge are the Top 3 protocols that have historically managed to attract demand to borrow on their protocols, with the first two being the only ones to have surpassed the $1B mark for loans taken. But as we can see in the graph above the story changes drastically from the summer of 2022 onwards, with these two protocols being the biggest losers. From the beginning of 2023 things start to change (for the better) for this particular sector, with Centrifuge with +$230M in active loans, Maple with +$130M and Goldfinch with +$100M.

🗒 Note that Maple suffered a hack that brought the protocol to ~$50M in defaulted loans and also the loss of important contributors to its protocol such as Celsius ($43M) and Alameda Research ($144M).

Defaulted Loans Amount:(August 2023)

Maple: $48,156,734

Centrifuge: $13,188,090

TrueFi: $4,437,820

There will be more detail on the causes and effects in the Financial Part 📊(Part 2).

As we have seen previously, the loans are mostly for Consumer ($184M) and Auto ($175M), which makes me think that they are not being productive loans and given that the average interest payment is high (10.67%), this may cause some kind of default in the different protocols. See this example 👀

‼ I don't really know the official destination of the loans. I may be wrongly assuming that the loans are unproductive and thus generate a certain type of insolvency at a certain point in time. This is where the protocols would undergo a necessary stress-test to prove their resilience and business model in the long term.

🇰🇪 Kenya → This country, with a total of 12 loans, is the most active borrower in Web3 protocols. With a total loans value of ~$74M historically, and +61$M in active loans for which it is paying 12.21% interest to the Goldfinch protocol. This money is mostly allocated to Auto, Carbon Projects and Fintech.

🇳🇬 Nigeria → The country with the 2º highest exposure to this loan type (RWA lending) with a total amount borrowed of +$70M and current loans worth +$56M. These loans are mostly offered by Goldfinch for which Nigeria is paying ~12.75% on average, with the majority of the money going to Carbon Projects, Consumer and Fintech.

🇲🇽 México→ Although Philippines is the third country with the most money in loans (+$53M), we will talk about Mexico(+$50,7M) as it is the country that allocates the money to distinct different sectors, in its case Agriculture, Carbon Project, Consumer, Energy, Fintech, Healthcare and Real State, with an average of +$5.6M per sector and payinga 12,75% of interest to carry out these projects to Goldfinch.

So far this is the first part on Real World Assets and their performance at DeFi. In the second part we will discuss financial data to get an idea of the financial health of these protocols and whether they have achieved PMF or are close to it. In addition I will show you a comparative analysis of returns and opportunities compared to native assets in DeFi.

Subscribe so you don't miss the 2º Part and stay tuned for the other quality reports I'm working on.

ftgdgf📊 Blockchain Analytics & Research 🔎 | M.D.V is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.